Page 348 - FY 2020-21 Blue Book Volume II

P. 348

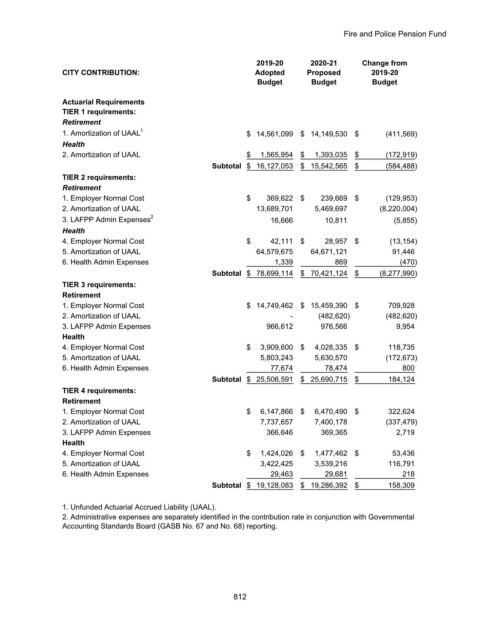

Fire and Police Pension Fund

2019-20 2020-21 Change from

CITY CONTRIBUTION: Adopted Proposed 2019-20

Budget Budget Budget

Actuarial Requirements

TIER 1 requirements:

Retirement

1. Amortization of UAAL 1 $ 14,561,099 $ 14,149,530 $ (411,569)

Health

2. Amortization of UAAL $ 1,565,954 $ 1,393,035 $ (172,919)

Subtotal $ 16,127,053 $ 15,542,565 $ (584,488)

TIER 2 requirements:

Retirement

1. Employer Normal Cost $ 369,622 $ 239,669 $ (129,953)

2. Amortization of UAAL 13,689,701 5,469,697 (8,220,004)

3. LAFPP Admin Expenses 2 16,666 10,811 (5,855)

Health

4. Employer Normal Cost $ 42,111 $ 28,957 $ (13,154)

5. Amortization of UAAL 64,579,675 64,671,121 91,446

6. Health Admin Expenses 1,339 869 (470)

Subtotal $ 78,699,114 $ 70,421,124 $ (8,277,990)

TIER 3 requirements:

Retirement

1. Employer Normal Cost $ 14,749,462 $ 15,459,390 $ 709,928

2. Amortization of UAAL - (482,620) (482,620)

3. LAFPP Admin Expenses 966,612 976,566 9,954

Health

4. Employer Normal Cost $ 3,909,600 $ 4,028,335 $ 118,735

5. Amortization of UAAL 5,803,243 5,630,570 (172,673)

6. Health Admin Expenses 77,674 78,474 800

Subtotal $ 25,506,591 $ 25,690,715 $ 184,124

TIER 4 requirements:

Retirement

1. Employer Normal Cost $ 6,147,866 $ 6,470,490 $ 322,624

2. Amortization of UAAL 7,737,657 7,400,178 (337,479)

3. LAFPP Admin Expenses 366,646 369,365 2,719

Health

4. Employer Normal Cost $ 1,424,026 $ 1,477,462 $ 53,436

5. Amortization of UAAL 3,422,425 3,539,216 116,791

6. Health Admin Expenses 29,463 29,681 218

Subtotal $ 19,128,083 $ 19,286,392 $ 158,309

1. Unfunded Actuarial Accrued Liability (UAAL).

2. Administrative expenses are separately identified in the contribution rate in conjunction with Governmental

Accounting Standards Board (GASB No. 67 and No. 68) reporting.

812