Page 330 - 2022-23 Blue Book Vol 2

P. 330

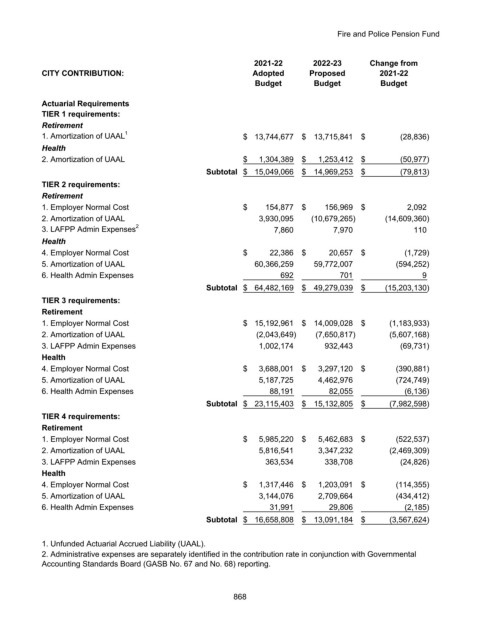

Fire and Police Pension Fund

2021-22 2022-23 Change from

CITY CONTRIBUTION: Adopted Proposed 2021-22

Budget Budget Budget

Actuarial Requirements

TIER 1 requirements:

Retirement

1. Amortization of UAAL 1 $ 13,744,677 $ 13,715,841 $ (28,836)

Health

2. Amortization of UAAL $ 1,304,389 $ 1,253,412 $ (50,977)

Subtotal $ 15,049,066 $ 14,969,253 $ (79,813)

TIER 2 requirements:

Retirement

1. Employer Normal Cost $ 154,877 $ 156,969 $ 2,092

2. Amortization of UAAL 3,930,095 (10,679,265) (14,609,360)

3. LAFPP Admin Expenses 2 7,860 7,970 110

Health

4. Employer Normal Cost $ 22,386 $ 20,657 $ (1,729)

5. Amortization of UAAL 60,366,259 59,772,007 (594,252)

6. Health Admin Expenses 692 701 9

Subtotal $ 64,482,169 $ 49,279,039 $ (15,203,130)

TIER 3 requirements:

Retirement

1. Employer Normal Cost $ 15,192,961 $ 14,009,028 $ (1,183,933)

2. Amortization of UAAL (2,043,649) (7,650,817) (5,607,168)

3. LAFPP Admin Expenses 1,002,174 932,443 (69,731)

Health

4. Employer Normal Cost $ 3,688,001 $ 3,297,120 $ (390,881)

5. Amortization of UAAL 5,187,725 4,462,976 (724,749)

6. Health Admin Expenses 88,191 82,055 (6,136)

Subtotal $ 23,115,403 $ 15,132,805 $ (7,982,598)

TIER 4 requirements:

Retirement

1. Employer Normal Cost $ 5,985,220 $ 5,462,683 $ (522,537)

2. Amortization of UAAL 5,816,541 3,347,232 (2,469,309)

3. LAFPP Admin Expenses 363,534 338,708 (24,826)

Health

4. Employer Normal Cost $ 1,317,446 $ 1,203,091 $ (114,355)

5. Amortization of UAAL 3,144,076 2,709,664 (434,412)

6. Health Admin Expenses 31,991 29,806 (2,185)

Subtotal $ 16,658,808 $ 13,091,184 $ (3,567,624)

1. Unfunded Actuarial Accrued Liability (UAAL).

2. Administrative expenses are separately identified in the contribution rate in conjunction with Governmental

Accounting Standards Board (GASB No. 67 and No. 68) reporting.

868