Page 290 - FY 2021-22 Blue Book Volume 2

P. 290

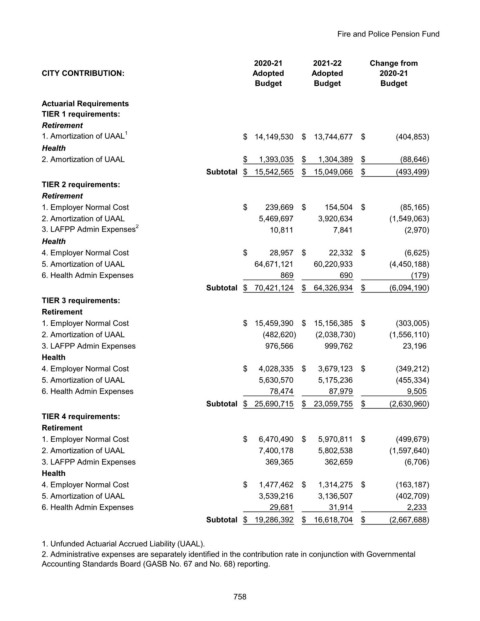

Fire and Police Pension Fund

2020-21 2021-22 Change from

CITY CONTRIBUTION: Adopted Adopted 2020-21

Budget Budget Budget

Actuarial Requirements

TIER 1 requirements:

Retirement

1. Amortization of UAAL 1 $ 14,149,530 $ 13,744,677 $ (404,853)

Health

2. Amortization of UAAL $ 1,393,035 $ 1,304,389 $ (88,646)

Subtotal $ 15,542,565 $ 15,049,066 $ (493,499)

TIER 2 requirements:

Retirement

1. Employer Normal Cost $ 239,669 $ 154,504 $ (85,165)

2. Amortization of UAAL 5,469,697 3,920,634 (1,549,063)

3. LAFPP Admin Expenses 2 10,811 7,841 (2,970)

Health

4. Employer Normal Cost $ 28,957 $ 22,332 $ (6,625)

5. Amortization of UAAL 64,671,121 60,220,933 (4,450,188)

6. Health Admin Expenses 869 690 (179)

Subtotal $ 70,421,124 $ 64,326,934 $ (6,094,190)

TIER 3 requirements:

Retirement

1. Employer Normal Cost $ 15,459,390 $ 15,156,385 $ (303,005)

2. Amortization of UAAL (482,620) (2,038,730) (1,556,110)

3. LAFPP Admin Expenses 976,566 999,762 23,196

Health

4. Employer Normal Cost $ 4,028,335 $ 3,679,123 $ (349,212)

5. Amortization of UAAL 5,630,570 5,175,236 (455,334)

6. Health Admin Expenses 78,474 87,979 9,505

Subtotal $ 25,690,715 $ 23,059,755 $ (2,630,960)

TIER 4 requirements:

Retirement

1. Employer Normal Cost $ 6,470,490 $ 5,970,811 $ (499,679)

2. Amortization of UAAL 7,400,178 5,802,538 (1,597,640)

3. LAFPP Admin Expenses 369,365 362,659 (6,706)

Health

4. Employer Normal Cost $ 1,477,462 $ 1,314,275 $ (163,187)

5. Amortization of UAAL 3,539,216 3,136,507 (402,709)

6. Health Admin Expenses 29,681 31,914 2,233

Subtotal $ 19,286,392 $ 16,618,704 $ (2,667,688)

1. Unfunded Actuarial Accrued Liability (UAAL).

2. Administrative expenses are separately identified in the contribution rate in conjunction with Governmental

Accounting Standards Board (GASB No. 67 and No. 68) reporting.

758