Page 39 - FY 2021-22 Supporting Information

P. 39

2021-22 PROPOSED BUDGET

PENSION AND RETIREMENT FUNDING POLICY

POLICY

If either the Los Angeles City Employees’ Retirement System or the Los Angeles Fire and Police

Pension System is greater than 100 percent funded, where the total annual required contribution

(adopted by their respective Boards) is less than the amount required to fund the normal cost of

retirement and health benefits for employees, then the City must limit the use of these savings in the

budget. Specifically, if the adopted contribution rate allows the City to contribute an amount less than

90 percent of the normal cost, this Policy prohibits the City from using these savings to fund the City’s

ongoing services and program costs. Instead, any savings or reduction in funding calculated due to the

incremental contribution rate below the 90 percent threshold will only be budgeted to pay down

unfunded pension or healthcare costs for retirees or, in the event that such costs are fully funded, as an

appropriation to the Budget Stabilization Fund. When the total UAAL is positive, the City will continue to

fully fund both the normal cost and UAAL as required by the City Charter.

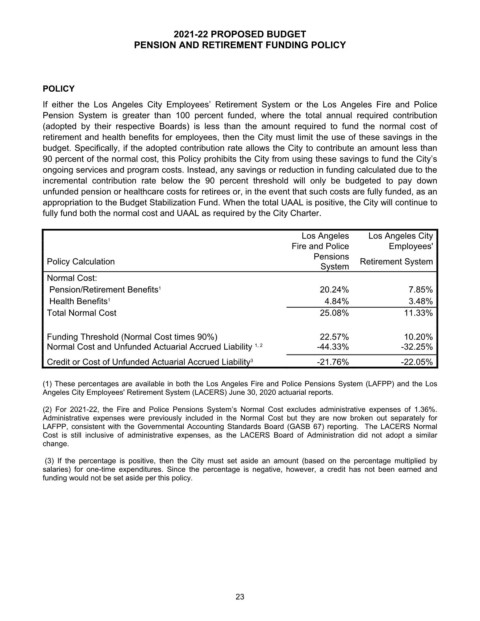

Los Angeles Los Angeles City

Fire and Police Employees'

Pensions

Policy Calculation Retirement System

System

Normal Cost:

Pension/Retirement Benefits 20.24% 7.85%

1

Health Benefits 4.84% 3.48%

1

Total Normal Cost 25.08% 11.33%

Funding Threshold (Normal Cost times 90%) 22.57% 10.20%

Normal Cost and Unfunded Actuarial Accrued Liability -44.33% -32.25%

1, 2

3

Credit or Cost of Unfunded Actuarial Accrued Liability -21.76% -22.05%

(1) These percentages are available in both the Los Angeles Fire and Police Pensions System (LAFPP) and the Los

Angeles City Employees' Retirement System (LACERS) June 30, 2020 actuarial reports.

(2) For 2021-22, the Fire and Police Pensions System’s Normal Cost excludes administrative expenses of 1.36%.

Administrative expenses were previously included in the Normal Cost but they are now broken out separately for

LAFPP, consistent with the Governmental Accounting Standards Board (GASB 67) reporting. The LACERS Normal

Cost is still inclusive of administrative expenses, as the LACERS Board of Administration did not adopt a similar

change.

(3) If the percentage is positive, then the City must set aside an amount (based on the percentage multiplied by

salaries) for one-time expenditures. Since the percentage is negative, however, a credit has not been earned and

funding would not be set aside per this policy.

23