Page 50 - FY 2022-23 Revenue Outlook

P. 50

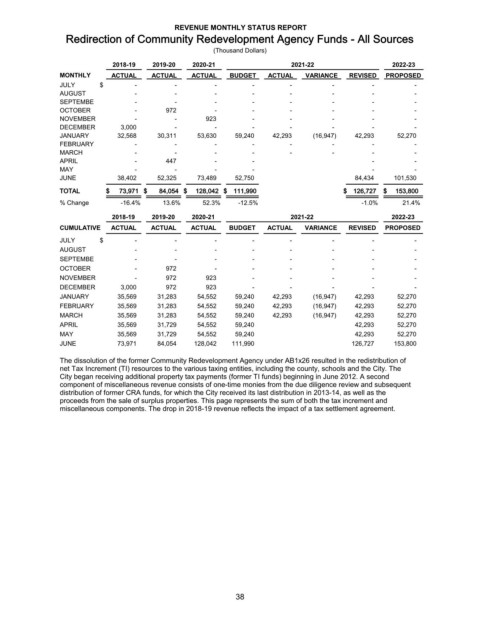

REVENUE MONTHLY STATUS REPORT

Redirection of Community Redevelopment Agency Funds - All Sources

(Thousand Dollars)

2018-19 2019-20 2020-21 2021-22 2022-23

MONTHLY ACTUAL ACTUAL ACTUAL BUDGET ACTUAL VARIANCE REVISED PROPOSED

JULY $ - - - - - - - -

AUGUST - - - - - - - -

SEPTEMBE - - - - - - - -

OCTOBER - 972 - - - - - -

NOVEMBER - - 923 - - - - -

DECEMBER 3,000 - - - - - - -

JANUARY 32,568 30,311 53,630 59,240 42,293 (16,947) 42,293 52,270

FEBRUARY - - - - - - - -

MARCH - - - - - - - -

APRIL - 447 - - - -

MAY - - - - - -

JUNE 38,402 52,325 73,489 52,750 84,434 101,530

TOTAL $ 73,971 $ 84,054 $ 128,042 $ 111,990 $ 126,727 $ 153,800

% Change -16.4% 13.6% 52.3% -12.5% -1.0% 21.4%

2018-19 2019-20 2020-21 2021-22 2022-23

CUMULATIVE ACTUAL ACTUAL ACTUAL BUDGET ACTUAL VARIANCE REVISED PROPOSED

JULY $ - - - - - - - -

AUGUST - - - - - - - -

SEPTEMBE - - - - - - - -

OCTOBER - 972 - - - - - -

NOVEMBER - 972 923 - - - - -

DECEMBER 3,000 972 923 - - - - -

JANUARY 35,569 31,283 54,552 59,240 42,293 (16,947) 42,293 52,270

FEBRUARY 35,569 31,283 54,552 59,240 42,293 (16,947) 42,293 52,270

MARCH 35,569 31,283 54,552 59,240 42,293 (16,947) 42,293 52,270

APRIL 35,569 31,729 54,552 59,240 42,293 52,270

MAY 35,569 31,729 54,552 59,240 42,293 52,270

JUNE 73,971 84,054 128,042 111,990 126,727 153,800

The dissolution of the former Community Redevelopment Agency under AB1x26 resulted in the redistribution of

net Tax Increment (TI) resources to the various taxing entities, including the county, schools and the City. The

City began receiving additional property tax payments (former TI funds) beginning in June 2012. A second

component of miscellaneous revenue consists of one-time monies from the due diligence review and subsequent

distribution of former CRA funds, for which the City received its last distribution in 2013-14, as well as the

proceeds from the sale of surplus properties. This page represents the sum of both the tax increment and

miscellaneous components. The drop in 2018-19 revenue reflects the impact of a tax settlement agreement.

38