Page 39 - 2020-21 Supporting Information Book_Revised

P. 39

2020-21 PROPOSED BUDGET

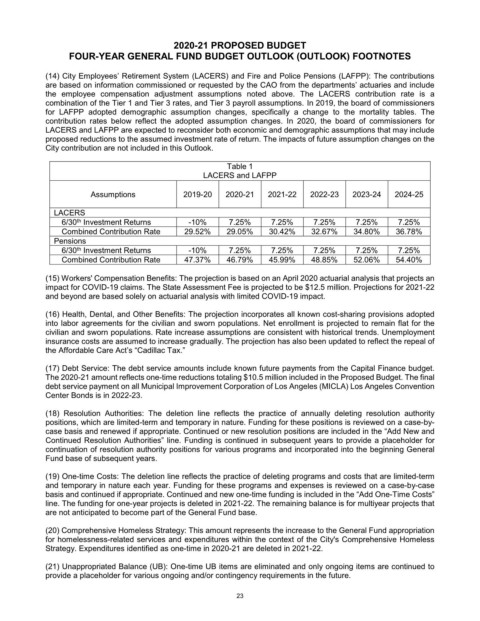

(14) City Employees’ Retirement System (LACERS) and Fire and Police Pensions (LAFPP): The contributions

are based on information commissioned or requested by the CAO from the departments’ actuaries and include

FOUR-YEAR GENERAL FUND BUDGET OUTLOOK (OUTLOOK) FOOTNOTES

the employee compensation adjustment assumptions noted above. The LACERS contribution rate is a

combination of the Tier 1 and Tier 3 rates, and Tier 3 payroll assumptions. In 2019, the board of commissioners

REVENUE:

(14) City Employees’ Retirement System (LACERS) and Fire and Police Pensions (LAFPP): The contributions

for LAFPP adopted demographic assumption changes, specifically a change to the mortality tables. The

are based on information commissioned or requested by the CAO from the departments’ actuaries and include

contribution rates below reflect the adopted assumption changes. In 2020, the board of commissioners for

(1) General Fund (GF) Base: The revenue base for each year represents the prior year’s estimated revenues.

the employee compensation adjustment assumptions noted above. The LACERS contribution rate is a

LACERS and LAFPP are expected to reconsider both economic and demographic assumptions that may include

combination of the Tier 1 and Tier 3 rates, and Tier 3 payroll assumptions. In 2019, the board of commissioners

proposed reductions to the assumed investment rate of return. The impacts of future assumption changes on the

(2) Revenue Growth: Revenue projections reflect the consensus of economists that the first quarter in 2020 will

for LAFPP adopted demographic assumption changes, specifically a change to the mortality tables. The

City contribution are not included in this Outlook.

mark the start of a recession, however, there is no consensus on its severity or length. Citing the relative good

contribution rates below reflect the adopted assumption changes. In 2020, the board of commissioners for

health of the pre-pandemic economy, higher state and local government reserves, and current stimulus efforts,

LACERS and LAFPP are expected to reconsider both economic and demographic assumptions that may include

Table 1

the Outlook assumes recovery in 2021. The current Safer at Home order is projected to end in May and the

proposed reductions to the assumed investment rate of return. The impacts of future assumption changes on the

LACERS and LAFPP

estimated receipts for 2020-21 and revenue growth for outgoing years reflect this assumption. The assumptions

City contribution are not included in this Outlook.

for economy sensitive revenues are also based on a single nonessential business closure event and no future

2022-23

2021-22

Assumptions

2023-24

2020-21

2024-25

2019-20

Safer at Home orders. The amounts represent projected incremental change to the base. Any one-time receipts

Table 1

are deducted from the estimated revenue growth for the following fiscal year.

LACERS and LAFPP

LACERS

7.25%

7.25%

7.25%

6/30 Investment Returns

-10%

7.25%

7.25%

th

The total projected revenue reflects above average growth in 2020-21 attributed to one-time receipts of delayed

2023-24

2024-25

2022-23

Assumptions

2021-22

2020-21

2019-20

29.05%

32.67%

36.78%

30.42%

34.80%

29.52%

Combined Contribution Rate

2019-20 payments and deferred tax collection efforts as well as a third quarter economic rebound. Outgoing years

Pensions

include average growth.

LACERS

6/30 Investment Returns -10% 7.25% 7.25% 7.25% 7.25% 7.25%

th

7.25%

7.25%

-10%

7.25%

6/30 Investment Returns

7.25%

th

7.25%

Combined Contribution Rate

45.99% historic growth for ensuing fiscal years.

47.37%

46.79%

(3) Property tax growth is projected at 6.6 percent for 2020-21 with 48.85% 52.06% 54.40%

36.78%

30.42%

Combined Contribution Rate

34.80%

29.52%

32.67%

29.05%

Documentary Transfer is a volatile revenue in particular when sales volume and price move together. The current

Pensions

year estimate assumes that pricing and sales volume hold steady, as the predicted recession is not being driven

(15) Workers' Compensation Benefits: The projection is based on an April 2020 actuarial analysis that projects an

7.25%

-10%

7.25%

th

7.25%

7.25%

6/30 Investment Returns

7.25%

by the housing market. Should pandemic-related layoffs result in permanent job loss, there is downside risk to this

impact for COVID-19 claims. The State Assessment Fee is projected to be $12.5 million. Projections for 2021-22

Combined Contribution Rate

52.06%

54.40%

48.85%

45.99%

47.37%

46.79%

revenue source as well. The Outlook includes steady growth in outgoing years as home prices are restrained by

and beyond are based solely on actuarial analysis with limited COVID-19 impact.

affordability. The Residential Development Tax is another volatile revenue which is being impacted by COVID-19

(15) Workers' Compensation Benefits: The projection is based on an April 2020 actuarial analysis that projects an

and the slowing of construction activity for new dwelling units. A significant rebound is expected in 2021-22 with

(16) Health, Dental, and Other Benefits: The projection incorporates all known cost-sharing provisions adopted

impact for COVID-19 claims. The State Assessment Fee is projected to be $12.5 million. Projections for 2021-22

into labor agreements for the civilian and sworn populations. Net enrollment is projected to remain flat for the

a return to gradual growth thereafter.

and beyond are based solely on actuarial analysis with limited COVID-19 impact.

civilian and sworn populations. Rate increase assumptions are consistent with historical trends. Unemployment

(4) Business tax revenue assumes the recovery of delayed 2019-20 receipts totaling $44.7 million in 2020-21.

insurance costs are assumed to increase gradually. The projection has also been updated to reflect the repeal of

(16) Health, Dental, and Other Benefits: The projection incorporates all known cost-sharing provisions adopted

Based on declines for previous recessions a 7 percent decrease is assumed for non-cannabis renewal activity.

the Affordable Care Act’s “Cadillac Tax.”

into labor agreements for the civilian and sworn populations. Net enrollment is projected to remain flat for the

Cannabis-related business activity assumes that current-year growth continues at 25 percent with no impact from

civilian and sworn populations. Rate increase assumptions are consistent with historical trends. Unemployment

the pandemic or recession. Total business tax growth for 2021-22 assumes recovery in non-cannabis business

(17) Debt Service: The debt service amounts include known future payments from the Capital Finance budget.

insurance costs are assumed to increase gradually. The projection has also been updated to reflect the repeal of

activity.

The 2020-21 amount reflects one-time reductions totaling $10.5 million included in the Proposed Budget. The final

the Affordable Care Act’s “Cadillac Tax.”

debt service payment on all Municipal Improvement Corporation of Los Angeles (MICLA) Los Angeles Convention

Sales tax growth is based on available economic forecasts and assumes a 5 percent decline for 2020-21 followed

Center Bonds is in 2022-23.

(17) Debt Service: The debt service amounts include known future payments from the Capital Finance budget.

by 3.8 percent average growth in the outgoing years. Subsequent to the formulation of this estimate, the State

The 2020-21 amount reflects one-time reductions totaling $10.5 million included in the Proposed Budget. The final

(18) Resolution Authorities: The deletion line reflects the practice of annually deleting resolution authority

extended the due date for the payment of quarterly sales tax owed by businesses. The reduction to City receipts

debt service payment on all Municipal Improvement Corporation of Los Angeles (MICLA) Los Angeles Convention

will be first realized before the close of 2019-20 and the impact from extended payment periods would continue

positions, which are limited-term and temporary in nature. Funding for these positions is reviewed on a case-by-

Center Bonds is in 2022-23.

until 2021-22.

case basis and renewed if appropriate. Continued or new resolution positions are included in the “Add New and

Continued Resolution Authorities” line. Funding is continued in subsequent years to provide a placeholder for

(18) Resolution Authorities: The deletion line reflects the practice of annually deleting resolution authority

(5) Electricity Users tax reflects an economic driven decline in 2020-21 consistent with estimates provided by the

continuation of resolution authority positions for various programs and incorporated into the beginning General

positions, which are limited-term and temporary in nature. Funding for these positions is reviewed on a case-by-

Department of Water and Power, reflecting current assumptions on rates and electricity consumption and adjusted

Fund base of subsequent years.

case basis and renewed if appropriate. Continued or new resolution positions are included in the “Add New and

to reflect uncollectable receipts which are expected to significantly increase as a result of the financial hardships

Continued Resolution Authorities” line. Funding is continued in subsequent years to provide a placeholder for

brought on by COVID-19. After a recovery in 2021-22, the outgoing years of revenue are consistent with historical

(19) One-time Costs: The deletion line reflects the practice of deleting programs and costs that are limited-term

continuation of resolution authority positions for various programs and incorporated into the beginning General

and temporary in nature each year. Funding for these programs and expenses is reviewed on a case-by-case

growth.

Fund base of subsequent years.

basis and continued if appropriate. Continued and new one-time funding is included in the “Add One-Time Costs”

The 2020-21 reduction in Gas Users tax revenue and no growth outlook is based on the full implementation of a

line. The funding for one-year projects is deleted in 2021-22. The remaining balance is for multiyear projects that

(19) One-time Costs: The deletion line reflects the practice of deleting programs and costs that are limited-term

taxpayer settlement agreement that reduces the tax base.

are not anticipated to become part of the General Fund base.

and temporary in nature each year. Funding for these programs and expenses is reviewed on a case-by-case

basis and continued if appropriate. Continued and new one-time funding is included in the “Add One-Time Costs”

The decline in Communications Users tax revenue continues due to aggressive wireless plan pricing and the

(20) Comprehensive Homeless Strategy: This amount represents the increase to the General Fund appropriation

line. The funding for one-year projects is deleted in 2021-22. The remaining balance is for multiyear projects that

decrease in landline use. Average declines of 7.9 percent are anticipated as part of the Outlook.

for homelessness-related services and expenditures within the context of the City's Comprehensive Homeless

are not anticipated to become part of the General Fund base.

Strategy. Expenditures identified as one-time in 2020-21 are deleted in 2021-22.

(20) Comprehensive Homeless Strategy: This amount represents the increase to the General Fund appropriation

(21) Unappropriated Balance (UB): One-time UB items are eliminated and only ongoing items are continued to

for homelessness-related services and expenditures within the context of the City's Comprehensive Homeless

provide a placeholder for various ongoing and/or contingency requirements in the future.

Strategy. Expenditures identified as one-time in 2020-21 are deleted in 2021-22.

(21) Unappropriated Balance (UB): One-time UB items are eliminated and only ongoing items are continued to

provide a placeholder for various ongoing and/or contingency requirements in the future.

21

23

23