Page 53 - FY 2022-23 Supporting Information

P. 53

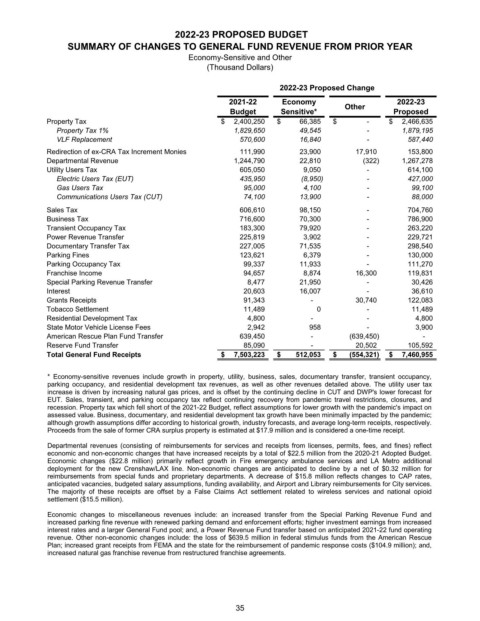

2022-23 PROPOSED BUDGET

SUMMARY OF CHANGES TO GENERAL FUND REVENUE FROM PRIOR YEAR

Economy-Sensitive and Other

(Thousand Dollars)

2022-23 Proposed Change

2021-22 Economy Other 2022-23

Budget Sensitive* Proposed

Property Tax $ 2,400,250 $ 66,385 $ - $ 2,466,635

Property Tax 1% 1,829,650 49,545 - 1,879,195

VLF Replacement 570,600 16,840 - 587,440

Redirection of ex-CRA Tax Increment Monies 111,990 23,900 17,910 153,800

Departmental Revenue 1,244,790 22,810 (322) 1,267,278

Utility Users Tax 605,050 9,050 - 614,100

Electric Users Tax (EUT) 435,950 (8,950) - 427,000

Gas Users Tax 95,000 4,100 - 99,100

Communications Users Tax (CUT) 74,100 13,900 - 88,000

Sales Tax 606,610 98,150 - 704,760

Business Tax 716,600 70,300 - 786,900

Transient Occupancy Tax 183,300 79,920 - 263,220

Power Revenue Transfer 225,819 3,902 - 229,721

Documentary Transfer Tax 227,005 71,535 - 298,540

Parking Fines 123,621 6,379 - 130,000

Parking Occupancy Tax 99,337 11,933 - 111,270

Franchise Income 94,657 8,874 16,300 119,831

Special Parking Revenue Transfer 8,477 21,950 - 30,426

Interest 20,603 16,007 - 36,610

Grants Receipts 91,343 - 30,740 122,083

Tobacco Settlement 11,489 0 - 11,489

Residential Development Tax 4,800 - - 4,800

State Motor Vehicle License Fees 2,942 958 - 3,900

American Rescue Plan Fund Transfer 639,450 - (639,450) -

Reserve Fund Transfer 85,090 - 20,502 105,592

Total General Fund Receipts $ 7,503,223 $ 512,053 $ (554,321) $ 7,460,955

* Economy-sensitive revenues include growth in property, utility, business, sales, documentary transfer, transient occupancy,

parking occupancy, and residential development tax revenues, as well as other revenues detailed above. The utility user tax

increase is driven by increasing natural gas prices, and is offset by the continuing decline in CUT and DWP's lower forecast for

EUT. Sales, transient, and parking occupancy tax reflect continuing recovery from pandemic travel restrictions, closures, and

recession. Property tax which fell short of the 2021-22 Budget, reflect assumptions for lower growth with the pandemic's impact on

assessed value. Business, documentary, and residential development tax growth have been minimally impacted by the pandemic;

although growth assumptions differ according to historical growth, industry forecasts, and average long-term receipts, respectively.

Proceeds from the sale of former CRA surplus property is estimated at $17.9 million and is considered a one-time receipt.

Departmental revenues (consisting of reimbursements for services and receipts from licenses, permits, fees, and fines) reflect

economic and non-economic changes that have increased receipts by a total of $22.5 million from the 2020-21 Adopted Budget.

Economic changes ($22.8 million) primarily reflect growth in Fire emergency ambulance services and LA Metro additional

deployment for the new Crenshaw/LAX line. Non-economic changes are anticipated to decline by a net of $0.32 million for

reimbursements from special funds and proprietary departments. A decrease of $15.8 million reflects changes to CAP rates,

anticipated vacancies, budgeted salary assumptions, funding availability, and Airport and Library reimbursements for City services.

The majority of these receipts are offset by a False Claims Act settlement related to wireless services and national opioid

settlement ($15.5 million).

Economic changes to miscellaneous revenues include: an increased transfer from the Special Parking Revenue Fund and

increased parking fine revenue with renewed parking demand and enforcement efforts; higher investment earnings from increased

interest rates and a larger General Fund pool; and, a Power Revenue Fund transfer based on anticipated 2021-22 fund operating

revenue. Other non-economic changes include: the loss of $639.5 million in federal stimulus funds from the American Rescue

Plan; increased grant receipts from FEMA and the state for the reimbursement of pandemic response costs ($104.9 million); and,

increased natural gas franchise revenue from restructured franchise agreements.

35