Page 23 - FY 2020-21 Revenue Outlook

P. 23

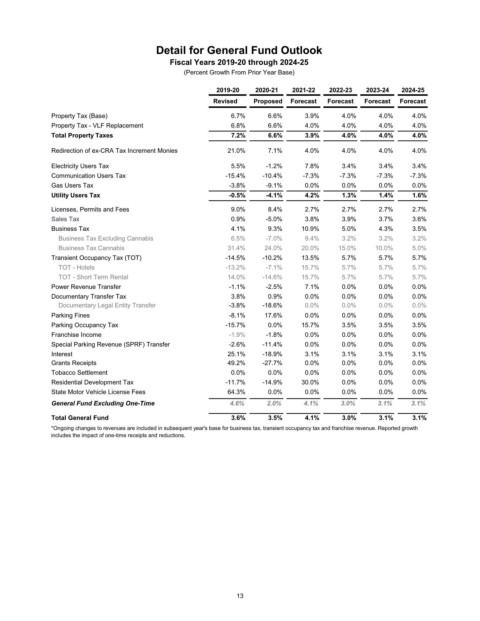

Detail for General Fund Outlook

Fiscal Years 2019-20 through 2024-25

(Percent Growth From Prior Year Base)

2019-20 2020-21 2021-22 2022-23 2023-24 2024-25

Revised Proposed Forecast Forecast Forecast Forecast

Property Tax (Base) 6.7% 6.6% 3.9% 4.0% 4.0% 4.0%

Property Tax - VLF Replacement 6.8% 6.6% 4.0% 4.0% 4.0% 4.0%

Total Property Taxes 7.2% 6.6% 3.9% 4.0% 4.0% 4.0%

Redirection of ex-CRA Tax Increment Monies 21.0% 7.1% 4.0% 4.0% 4.0% 4.0%

Electricity Users Tax 5.5% -1.2% 7.8% 3.4% 3.4% 3.4%

Communication Users Tax -15.4% -10.4% -7.3% -7.3% -7.3% -7.3%

Gas Users Tax -3.8% -9.1% 0.0% 0.0% 0.0% 0.0%

Utility Users Tax -0.5% -4.1% 4.2% 1.3% 1.4% 1.6%

Licenses, Permits and Fees 9.0% 8.4% 2.7% 2.7% 2.7% 2.7%

Sales Tax 0.9% -5.0% 3.8% 3.9% 3.7% 3.6%

Business Tax 4.1% 9.3% 10.9% 5.0% 4.3% 3.5%

Business Tax Excluding Cannabis 6.5% -7.0% 9.4% 3.2% 3.2% 3.2%

Business Tax Cannabis 31.4% 24.0% 20.0% 15.0% 10.0% 5.0%

Transient Occupancy Tax (TOT) -14.5% -10.2% 13.5% 5.7% 5.7% 5.7%

TOT - Hotels -13.2% -7.1% 15.7% 5.7% 5.7% 5.7%

TOT - Short Term Rental 14.0% -14.6% 15.7% 5.7% 5.7% 5.7%

Power Revenue Transfer -1.1% -2.5% 7.1% 0.0% 0.0% 0.0%

Documentary Transfer Tax 3.8% 0.9% 0.0% 0.0% 0.0% 0.0%

Documentary Legal Entity Transfer -3.8% -18.6% 0.0% 0.0% 0.0% 0.0%

Parking Fines -8.1% 17.6% 0.0% 0.0% 0.0% 0.0%

Parking Occupancy Tax -15.7% 0.0% 15.7% 3.5% 3.5% 3.5%

Franchise Income -1.9% -1.8% 0.0% 0.0% 0.0% 0.0%

Special Parking Revenue (SPRF) Transfer -2.6% -11.4% 0.0% 0.0% 0.0% 0.0%

Interest 25.1% -18.9% 3.1% 3.1% 3.1% 3.1%

Grants Receipts 49.2% -27.7% 0.0% 0.0% 0.0% 0.0%

Tobacco Settlement 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Residential Development Tax -11.7% -14.9% 30.0% 0.0% 0.0% 0.0%

State Motor Vehicle License Fees 64.3% 0.0% 0.0% 0.0% 0.0% 0.0%

General Fund Excluding One-Time 4.6% 2.0% 4.1% 3.0% 3.1% 3.1%

Total General Fund 3.6% 3.5% 4.1% 3.0% 3.1% 3.1%

*Ongoing changes to revenues are included in subsequent year's base for business tax, transient occupancy tax and franchise revenue. Reported growth

includes the impact of one-time receipts and reductions.

13