Page 74 - FY 2020-21 Revenue Outlook

P. 74

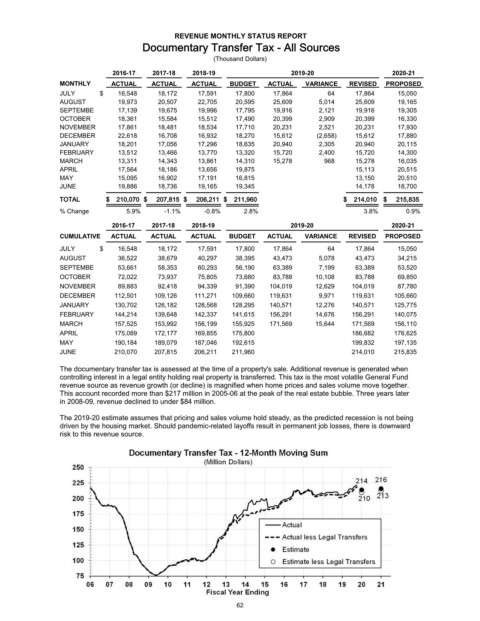

REVENUE MONTHLY STATUS REPORT

Documentary Transfer Tax - All Sources

(Thousand Dollars)

2016-17 2017-18 2018-19 2019-20 2020-21

MONTHLY ACTUAL ACTUAL ACTUAL BUDGET ACTUAL VARIANCE REVISED PROPOSED

JULY $ 16,548 18,172 17,591 17,800 17,864 64 17,864 15,050

AUGUST 19,973 20,507 22,705 20,595 25,609 5,014 25,609 19,165

SEPTEMBE 17,139 19,675 19,996 17,795 19,916 2,121 19,916 19,305

OCTOBER 18,361 15,584 15,512 17,490 20,399 2,909 20,399 16,330

NOVEMBER 17,861 18,481 18,534 17,710 20,231 2,521 20,231 17,930

DECEMBER 22,618 16,708 16,932 18,270 15,612 (2,658) 15,612 17,880

JANUARY 18,201 17,056 17,296 18,635 20,940 2,305 20,940 20,115

FEBRUARY 13,512 13,466 13,770 13,320 15,720 2,400 15,720 14,300

MARCH 13,311 14,343 13,861 14,310 15,278 968 15,278 16,035

APRIL 17,564 18,186 13,656 19,875 15,113 20,515

MAY 15,095 16,902 17,191 16,815 13,150 20,510

JUNE 19,886 18,736 19,165 19,345 14,178 18,700

TOTAL $ 210,070 $ 207,815 $ 206,211 $ 211,960 $ 214,010 $ 215,835

% Change 5.9% -1.1% -0.8% 2.8% 3.8% 0.9%

2016-17 2017-18 2018-19 2019-20 2020-21

CUMULATIVE ACTUAL ACTUAL ACTUAL BUDGET ACTUAL VARIANCE REVISED PROPOSED

JULY $ 16,548 18,172 17,591 17,800 17,864 64 17,864 15,050

AUGUST 36,522 38,679 40,297 38,395 43,473 5,078 43,473 34,215

SEPTEMBE 53,661 58,353 60,293 56,190 63,389 7,199 63,389 53,520

OCTOBER 72,022 73,937 75,805 73,680 83,788 10,108 83,788 69,850

NOVEMBER 89,883 92,418 94,339 91,390 104,019 12,629 104,019 87,780

DECEMBER 112,501 109,126 111,271 109,660 119,631 9,971 119,631 105,660

JANUARY 130,702 126,182 128,568 128,295 140,571 12,276 140,571 125,775

FEBRUARY 144,214 139,648 142,337 141,615 156,291 14,676 156,291 140,075

MARCH 157,525 153,992 156,199 155,925 171,569 15,644 171,569 156,110

APRIL 175,089 172,177 169,855 175,800 186,682 176,625

MAY 190,184 189,079 187,046 192,615 199,832 197,135

JUNE 210,070 207,815 206,211 211,960 214,010 215,835

The documentary transfer tax is assessed at the time of a property's sale. Additional revenue is generated when

controlling interest in a legal entity holding real property is transferred. This tax is the most volatile General Fund

revenue source as revenue growth (or decline) is magnified when home prices and sales volume move together.

This account recorded more than $217 million in 2005-06 at the peak of the real estate bubble. Three years later

in 2008-09, revenue declined to under $84 million.

The 2019-20 estimate assumes that pricing and sales volume hold steady, as the predicted recession is not being

driven by the housing market. Should pandemic-related layoffs result in permanent job losses, there is downward

risk to this revenue source.

62