Page 20 - FY 2022-23 Revenue Outlook

P. 20

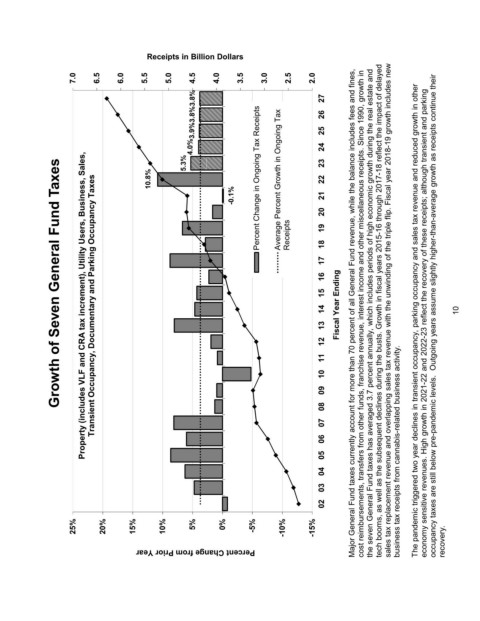

Growth of Seven General Fund Taxes

25% 7.0

Property (includes VLF and CRA tax increment), Utility Users, Business, Sales,

Transient Occupancy, Documentary and Parking Occupancy Taxes 6.5

20%

6.0

15% 10.8% 5.5

Percent Change from Prior Year 5% 5.3% 4.0% 3.9%3.8%3.8% 4.5 Receipts in Billion Dollars

10%

5.0

4.0

0%

-0.1%

-5%

Percent Change in Ongoing Tax Receipts 3.5

3.0

Average Percent Growth in Ongoing Tax

-10%

Receipts 2.5

-15% 2.0

02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27

Fiscal Year Ending

Major General Fund taxes currently account for more than 70 percent of all General Fund revenue, while the balance includes fees and fines,

cost reimbursements, transfers from other funds, franchise revenue, interest income and other miscellaneous receipts. Since 1990, growth in

the seven General Fund taxes has averaged 3.7 percent annually, which includes periods of high economic growth during the real estate and

tech booms, as well as the subsequent declines during the busts. Growth in fiscal years 2015-16 through 2017-18 reflect the impact of delayed

sales tax replacement revenue and overlapping sales tax revenue with the unwinding of the triple flip. Fiscal year 2018-19 growth includes new

business tax receipts from cannabis-related business activity.

The pandemic triggered two year declines in transient occupancy, parking occupancy and sales tax revenue and reduced growth in other

economy sensitive revenues. High growth in 2021-22 and 2022-23 reflect the recovery of these receipts; although transient and parking

occupancy taxes are still below pre-pandemic levels. Outgoing years assume slightly higher-than-average growth as receipts continue their

recovery.

10