Page 27 - 2020-21 Supporting Information Book_Revised

P. 27

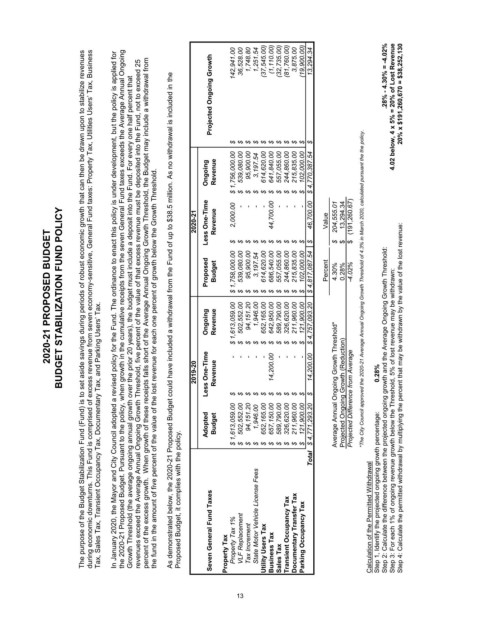

Annual Ongoing not to exceed 25 Projected Ongoing Growth $ 142,941.00 $ 36,528.00 $ 1,748.80 $ 1,251.54 $ (37,545.00) $ (1,110.00) $ (32,735.00) $ (81,760.00)

can then be drawn upon to stabilize revenues

Fund taxes exceeds the Average For every one half percent that into the Fund, deposited Ongoing Revenue $ 1,756,000.00 $ 539,080.00 $ 95,900.00 $ 3,197.54 $ 614,620.00 $ 641,840.00 $ 557,055.00 $ 244,860.00 $ 215,835.00 $ 102,000.00 $ 4,770,387.54

revenues exceed the Average Annual Ongoing Growth Threshold, five percent of the value of that excess revenue must be

that deposit into the Fund. Average Annual Ongoing Growth Threshold, the Budget may include a withdrawal from 2020-21 Less One-Time Revenue $ 2,000.00 $ - $ - $ - $ - $ 44,700.00 $ - $ - $ - $ - $ 46,700.00 Value $ 204,555.01 $ 13,294.3

the 2020-21 Proposed Budget. Pursuant to the policy, when growth in the cumulative receipts from the seven General

The purpose of the Budget Stabilization Fund (Fund) is to set aside savings during periods of robust economic growth

2020-21 PROPOSED BUDGET BUDGET STABILIZATION FUND POLICY This Fund is comprised of excess revenue from seven economy-sensitive, General Fund taxes: Property Tax, Utilities Users’ Tax, Business the Mayor and City Council adopted a revised policy for the Fund. The ordinance to enact this policy is under development, but the policy is applied for budget must include a of the lost revenue for each one percent of growth below the Growth Threshold. 2020-21 Proposed Budget

Tax, Sales Tax, Transient Occupancy Tax, Documentary Tax, and Parking Users’ Tax.

Growth Threshold (the average ongoing annual growth over the prior 20 years), the

When growth of these receipts falls short of the

2019-20 Less One-Time Revenue $ - $ - $ - $ - $ - $ 14,200.00 $ - $ - $ - $ - $ 14,200.00 Average Annual Ongoing Growth Threshold* Projected Ongoing Growth (Reduction) Projected Difference from Average 0.28% S

Adopted Budget $ 1,613,059.00 $ 502,552.00 $ 94,151.20 $ 1,946.00 $ 652,165.00 $ 657,150.00 $ 589,790.00 $ 326,620.00 $ 211,960.00 $ 121,900.00 $ 4,771,293.20 Step 2: Calculate the difference between the projected ongoing growth and the Average Ongoing Growth Threshold: Step 3: For each 1% of ongoing revenue growth below the Threshold, 5% of lost revenue may be wi

Total

during economic downturns. In January 2020, of the excess growth. percent the fund in the amount of five percent of the value As demonstrated below, the Proposed Budget, it complies with the policy. Seven General Fund Taxes Property Tax Property Tax 1% VLF Replacement Tax Increment State Motor Vehicle License Fees Utility Users Tax Business Tax Sales Tax Transient Occupancy Tax Documentary Transfer Tax Parking Occupancy Tax

13